AEPS | BBPS | API | White Label Solution | Money Transfer | Pan card UTI PSA | Recharge and Bill Payment | Travel Solutions | Software Solutions | Digital Marketing

AEPS | BBPS | API | White Label Solution | Money Transfer | Pan card UTI PSA | Recharge and Bill Payment | Travel Solutions | Software Solutions | Digital Marketing

CSP stands for Customer Service Point. It refers to a model where banks or financial institutions appoint agents or third-party entities to provide basic banking services to customers in remote or underserved areas where establishing a full-fledged branch may not be feasible. These CSPs act as intermediaries, offering services like account opening, deposits, withdrawals, fund transfers, and other basic banking transactions on behalf of the bank. They help extend banking services to a wider population, especially in rural areas, thereby promoting financial inclusion.

Bank BC stands for Bank Business Correspondent. These are individuals or entities appointed by banks to provide banking and financial services on their behalf, especially in remote or underserved areas where traditional banking infrastructure may be lacking. BCs act as intermediaries between the bank and customers, offering services such as account opening, cash deposits, withdrawals, fund transfers, loan disbursement, and other basic banking transactions. They play a crucial role in extending banking services to unbanked or underbanked populations, thereby promoting financial inclusion.

Bank Business Correspondents (BCs) offer a range of services on behalf of banks, typically in areas where traditional banking infrastructure is limited. Some common services provided by BCs include:

Account Opening: BCs assist customers in opening bank accounts, including savings accounts, current accounts, and other types of accounts offered by the bank.

Cash Deposits: BCs accept cash deposits from customers into their bank accounts, allowing them to securely store their funds.

Cash Withdrawals: Customers can withdraw cash from their bank accounts through BCs, providing convenient access to their funds.

Fund Transfers: BCs facilitate fund transfers between accounts, including within the same bank or to accounts in other banks.

Balance Inquiry: Customers can check their account balance through BCs, allowing them to monitor their finances conveniently.

Mini-Statements: BCs provide mini-statements to customers, offering a summary of recent transactions and account activity.

Loan Application Processing: Some BCs assist customers in applying for loans offered by the bank, including personal loans, business loans, or agricultural loans.

Insurance Sales: In some cases, BCs may also offer insurance products on behalf of the bank, such as life insurance or health insurance policies.

These services help extend banking access to underserved populations, promoting financial inclusion and allowing individuals to participate more fully in the formal financial system.

PNB CSP refers to the PNB (Punjab National Bank) Customer Service Point. PNB is a major public sector bank in India, and CSP refers to the establishment of Customer Service Points or banking outlets by PNB in partnership with individuals or entities.

PNB CSP allows individuals or entities to become authorized agents of the bank and offer basic banking services to customers in areas where the bank may not have a physical branch. These CSPs act as an extension of the bank and provide services such as account opening, cash deposit and withdrawal, fund transfers, balance inquiry, and other banking services.

The objective of PNB CSP is to enhance banking accessibility and reach remote or underserved areas where setting up full-fledged branches may not be feasible. It helps in promoting financial inclusion by bringing banking services closer to the customers.

To become a PNB CSP, interested individuals or entities typically need to meet certain eligibility criteria set by the bank. These criteria may include factors such as financial stability, infrastructure, experience in financial services, and adherence to regulatory guidelines. The exact process and requirements may vary, and it’s advisable to reach out to PNB directly or visit their official website for detailed information on becoming a PNB CSP.

Please note that the information provided here is based on general knowledge and the banking landscape as of my knowledge cutoff in September 2021. It’s recommended to verify the current details and requirements with PNB directly or through their official channels.

The commission structure for PNB Customer Service Points (CSPs) may vary and is subject to the policies and agreements between Punjab National Bank (PNB) and the CSPs. The specific commission rates and structure can be obtained by contacting PNB directly or referring to their official communication channels.

PNB typically provides commission or fees to CSPs for the various banking services they offer on behalf of the bank. These services may include account opening, cash deposit and withdrawal, fund transfers, balance inquiry, and other basic banking transactions.

The commission rates may depend on factors such as the type of transaction, transaction volume, location, and the CSP’s performance. PNB may have different commission structures for different types of CSPs, such as individual agents, banking correspondents, or business correspondents.

To obtain accurate and up-to-date information about the commission rates and structure for PNB CSPs, it is recommended to contact PNB’s designated department or visit their official website for the specific details and terms applicable to your situation.

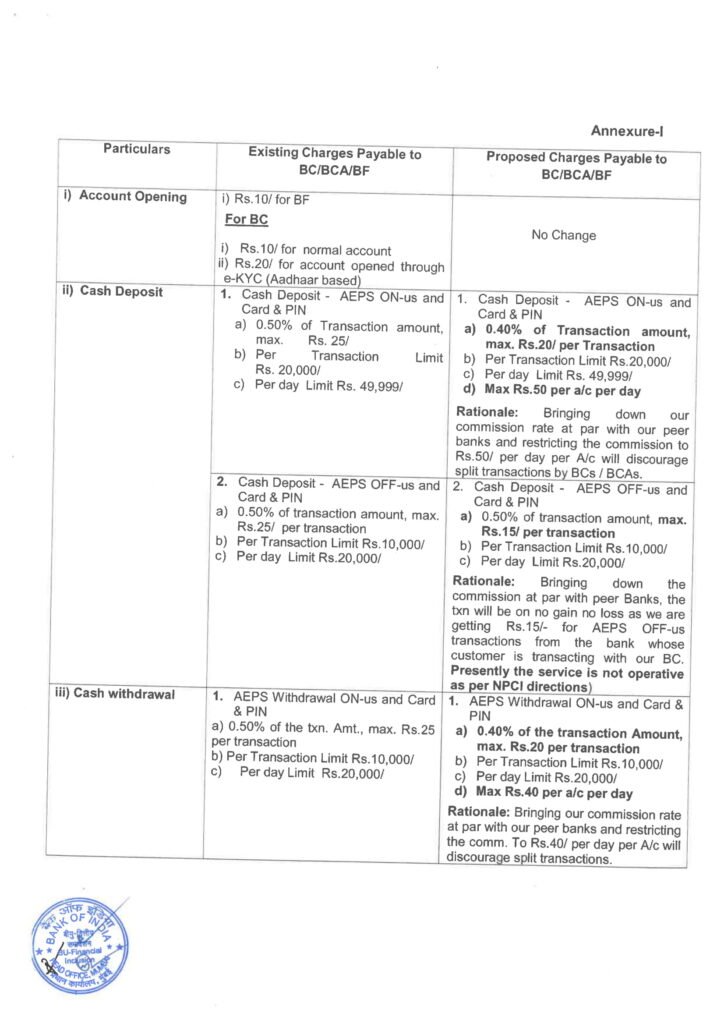

80% of fee recovered from customers, Minimum Rs. 8/-, Maximum Rs.80/- (1% of amount remitted, Min. Rs. 10/- & Max. Rs. 100/- recovered from the customers)

Up to Rs. 10,000/-: 0.25% Min Rs. 2/- Max Rs. 8/-

Up to Rs. 10,000/-: 0.25% Min Rs.2/- Max Rs. 10/-

Rs. 10,001/- to Rs.15,000/-: Rs. 10/-

Rs. 10,001/- to Rs.15,000/- : Rs. 12/-

Rs. 15,001/- to Rs.20,000/-: Rs. 12/- (No recovery from customers)

Rs. 15,001/- to Rs.20,000/-: Rs. 15/- (No recovery fromcustomers)

(Rationale: There is no distinction betweenHome & Non-Home customers. Doing away with recovery from customers will give a boost to migrating customers from Br. To CSPs.)

(Rationale: There is no distinction between Home & Non-Home customers. Doing away with recovery from customers will give a boost to migrating customers from Br. To CSPs.)

7

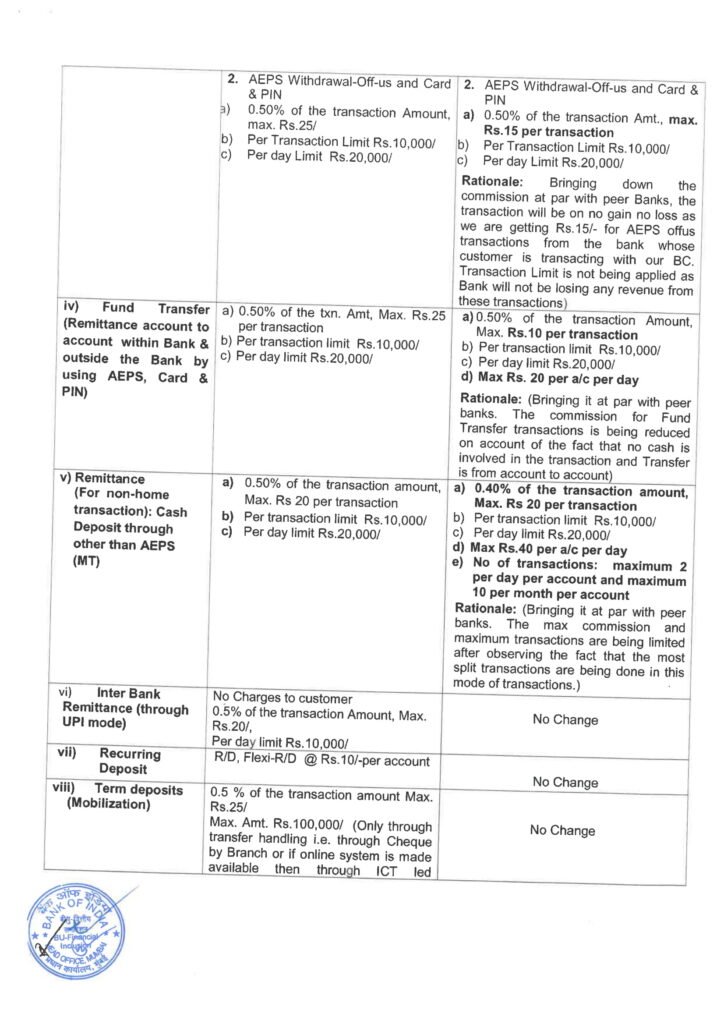

Remittance (Transfer) (Home Branch A/Cs)

Up to Rs.10,000/-: 1% of the amount, Min.Rs.3/-, Max Rs.10/-

No change

Up to Rs.10,000/-: 1% of the amount, Min.Rs.3/-, Max Rs.12/-

Rs.10,001/- to Rs.15,000/-: Rs.12/-

Rs.10,001/- to Rs.15,000/-: Rs.15/-

Rs.15,001/- to Rs.20,000/-: Rs.15/-

Rs.15,001/- to Rs.20,000/-: Rs.17/-

8

Remittance (Transfer) (Non- Home Branch A/Cs)

50% of fee recovered from customers, Minimum Rs.5/- , Maximum Rs.50/-

Up to Rs.10,000/-: 1% of the amount, Min.Rs.3/- , Max Rs.10/-

Up to Rs.10,000/-: 1% of the amount, Min.Rs.3/-, Max Rs.12/-

(1% of amount remitted, Min. Rs. 10/- & Max. Rs. 100/- recovered from the customers)

Rs.10,001/- to Rs.15,000/-: Rs.12/-

Rs.10,001/- to Rs.15,000/-: Rs. 15/-

Rs.15,001/- to Rs.20,000/-: Rs.15/- (No recovery from customers)

Rs.15,001/- to Rs.20,000/-: Rs. 17/- (No recovery fromcustomers)

(Rationale: There is no distinction betweenHome & Non-Home customers. Doing away with recovery from customers will give a boost to migrating customers from Br. To CSPs.)

(Rationale: There is no distinction between Home & Non-Home customers. Doing away with recovery from customers will give a boost to migrating customers from Br. ToCSPs.)

S.N.

Particulars

Existing

ProposedRural/Semi Urban

ProposedUrban / Metro

9.a

IMPS (Cash) (Up to Rs.5,000/-)(Recovery from customers: 1.25% of amount remitted, Min. Rs. 24/- & Max. Rs. 100/-)

80% of fee recovered from customers, Minimum – Rs.8/- & Maximum – Rs.28/-

(Cash up to Rs.10,000/-) 80% of fee recovered from customers, Minimum – Rs.8/- & Maximum – Rs.35/-

(Cash up to Rs.10,000/-) 80% of fee recovered from customers, Minimum – Rs.8/- & Maximum – Rs.40/-

9.b

IMPS (Transfer) (up to Rs.20,000/-)(Recovery from customers: 1.25% of amount remitted, Min. Rs. 24/- & Max. Rs. 100/-)

50% of fee recovered from customers, Minimum – Rs.5/- & Maximum – Rs.50/-

No change

50% of fee recovered from customers, Minimum – Rs.5/- & Maximum – Rs.60/-

10

Bill Collection Service (BBPS) 1. Utilities (Electricity, Gas and Water.

i) Up to Rs. 1000/- 80% of CCF earned i.e. Rs. 4/- per bill ii) Above Rs. 1000/- 80% of CCF earned i.e. Rs. 12/- per bill

(Recovery from customers: Up to Rs. 1000/-: Rs. 5/- & Above Rs. 1000/-: Rs. 15/- per bill, NIL for DTH).

S.N.

Particulars

Existing

ProposedRural/Semi Urban

ProposedUrban / Metro

11

a) Rural CSP (Incentive)

Rs.2000/- subject to opening minimum 50 accounts per month or minimum 100 transactions per month or both.

No Change

NAP

Payment of incentive for all CSPs at LWE / Aspirational districts and State of Sikkim Rs. 3000/- per month as incentive or the actual commission including Rural Commission payable as per the applicable fee structure for the BC Channel, whichever is higher. Condition: CSPs operating in Aspirational Districts (as notified by NITI Ayog, GOI) and in the State of Sikkim are required to undertake a minimum number of 25 transactions during the month.Minimum number of transactions is not applicable to LWE districts.

No Change

NAP

Payment of incentive for CSPs (other than Urban CSPs) of North Eastern States Rs. 4000/- per month as incentive or the actual commission including Rural Commission payable as per the applicable fee structure for the BC Channel, whichever is higher Condition: CSPs operating in North Eastern States (Rural & semi urban) are required to undertake a minimum of 25 transactions during the month.

No Change

NAP

S.N.

Particulars

Existing

ProposedRural/Semi Urban

ProposedUrban / Metro

12

Weekly average balance maintenance fee (each CSP) (Min. 200 no. of BSBD accounts)

1.00% p.a. for average balance > Rs.1,700/- Balances held in account up to Rs.5,00,000/- only will be considered for calculation of incentive against average balance maintenance fee.Maximum commission for maintenance of average balance for each CSP will be capped at Rs. 25000/- per month inclusive of GST.Minimum no of transactions during the month – RU/SU – 100, UR/Metro – 200.

i) 1.10% per annum for average balance > Rs. 2000/-, subject to following conditions: Balances held in account up to Rs.5,00,000/- only will be considered for calculation of incentive against average balance maintenance fee.Maximum commission for maintenance of average balance for each CSP will be capped at Rs. 25000/- per month inclusive of GST.Minimum no of transactions during the month – RU/SU – 100, UR/Metro – 200.Rationale:Average balance in the channel is Rs. 2,523/- per account as on 28.02.2021.Only active CSPs to get advantage.

Same as applicable to Rural/Semi-urban category

13

Non-zero balance account (each CSP) (Min. 200 no. of accounts & minimum 25transactions during the month)

i Less than 85% – Nil

NIL Rationale:Zero balance accounts as on 28.02.2021 are now only 2% (27.48 lacs a/cs) out of the total no. of 1373 lacs accounts.Incentive is being paid even though SB accounts are opened with zero balance. Further, incentives are also paid on weekly average balance. Commission on non – zero balance accounts is proposed to be done away with on portfolio basis, which will avoid multipleincentivisation.

Same as applicable to Rural/Semi-urban category

ii) 85% and above – Rs.750/- per month

iii 90% and above -Rs1000/- per month

Nonzero (funded) accounts having monthly average balance of Rs.100/- & above, Minimum 100 transactions during the month at rural / semi urban centre and 200 transactions at urban / metro centres

14

Aadhaar seeding (existing account holders)

Rs. 5/- per account

No change

Same as applicable to Rural/Semi-urban category

15

Mobile Seeding: (Inputting Valid Contact Number)

Rs. 5/- per account

No change

Same as applicable to Rural/Semi-urban category

S.N.

Particulars

Existing

ProposedRural/Semi Urban

ProposedUrban / Metro

16

Generating Green PIN for RuPay ATM Cards

Rs.5/- per PIN reset per Account / Month (For first time PIN generation)

No change

Same as applicable to Rural/Semi-urban category

17

Mini Statement through Micro ATM (Maximum 2 mini statement per account per month)

Rs. 2/- per statement

No change

Same as applicable to Rural/Semi-urban category

18

Passbook printing

Rs.5/- per passbook per day.Rs.6/- per passbook per day beyond 300 passbooks printing.

Rs.5/- per passbook per day. Condition:(Max. 05 times per a/c in a month)

Rs.6/- per passbook per day. Condition:(Max. 05 times per a/c in a month)

19

Social Security Scheme PMJJBY.PMSBY.APY. (Premium on enrolment to be collected from customers, as per Annexure -II enclosed)

a) Rs.30.00/- b) Rs.1.00/- c) Rs.80.00/- to Rs. 100/- (Depending on number of enrolments) (Govt. mandated)

No change

Same as applicable to Rural/Semi-urban category

Services being rolled out soon

20

Request for issuance of cheque book of 10 leaves (Non FI customers with AEPS) (Recovery from customers: First 10 cheque leaves free in a financial year at branch, thereafter: 10 leaf cheque Book at Rs. 40/- + GST & 25 leaf cheque Book at Rs. 75/- + GST)

—

Rs. 5/-

Rs. 6/-

21

Request for Stop cheque (Recovery from customers: Rs. 100/- + GST per instrument maximum Rs. 500/- + GST per instance)

—

Rs.2/- per instruments – Max. Rs. 5/-

Same as applicable to Rural/Semi-urban category

22

Request for Blocking of (RuPay/ATM) Card

—

Rs. 2/- per instance

Same as applicable to Rural/Semi-urban category

S.N.

Particulars

Existing

ProposedRural/Semi Urban

ProposedUrban / Metro

23

NEFT by transfer up to Rs. 10,000/- (Both FI and Non FI customers) (Recovery from customers: Up to Rs. 10000/-: Rs. 2/- + GST,AboveRs. 10000/-: Rs. 4/-+ GST)

—

Rs. 2/- per transfer

Same as applicable to Rural/Semi-urban category

24

Deposit in Loan Accounts

Un – Mapped accounts

0.40% Min. Rs.2/-, Max Rs. 10/-

No change

Same as applicable to Rural/Semi-urban category

Mapped accounts

0.50% of collections made/routed by BCs/CSPs

No change

Same as applicable to Rural/Semi-urban category

As an AI language model, I don’t have access to real-time information or the ability to provide up-to-date commission structures. The commission structure for SBI (State Bank of India) CSP (Customer Service Point) may vary over time and can depend on various factors, including the specific agreement between SBI and the CSP.

To obtain the most accurate and current commission structure for SBI CSP, I recommend reaching out to the nearest SBI branch or contacting SBI directly. They will be able to provide you with the most up-to-date information on the commission rates, structure, and any other relevant details regarding becoming a CSP for SBI.

To register as a CSP (Customer Service Point) for SBI (State Bank of India), you can follow these general steps:

Contact SBI Branch: Reach out to the nearest SBI branch or the branch of your preference. Inquire about the process and requirements for becoming a CSP. The branch manager or designated official will guide you through the registration process.

Fulfill Eligibility Criteria: Ensure that you meet the eligibility criteria set by SBI for CSP registration. These criteria may include factors such as age, educational qualifications, experience in the banking sector, and other requirements specified by the bank.

Gather Required Documents: Collect the necessary documents for the registration process. These documents may include:

Application form: Obtain the CSP application form from the SBI branch or download it from their official website.

Identity proof: Provide documents such as Aadhaar card, PAN card, voter ID, or passport as proof of identity.

Address proof: Submit documents like utility bills, rent agreement, or bank statements as proof of address.

Educational qualifications: Provide certificates or documents that validate your educational qualifications.

Experience certificates: If applicable, submit experience certificates or letters from previous employers to showcase your experience in the banking or financial sector.

Other documents: SBI may require additional documents as per their specific requirements, so it’s advisable to check with the branch for a comprehensive list.

Submit Application: Complete the CSP application form and attach all the required documents. Submit the application form along with the documents to the SBI branch. Ensure that the application is filled accurately and all the supporting documents are provided.

Verification and Approval: SBI will review your application and conduct the necessary verification checks. This process may involve background checks, due diligence, and assessing your suitability as a CSP. If your application is approved, you will be notified by the bank.

Agreement and Training: Once approved, you may be required to sign an agreement with SBI, outlining the terms and conditions of the CSP arrangement. SBI may also provide training on their products, services, and operating procedures. Attend the training sessions and familiarize yourself with the necessary guidelines.

Infrastructure Setup: Set up the required infrastructure at your CSP location. This may include setting up a computer system, internet connectivity, biometric devices (if applicable), and other necessary equipment as per the guidelines provided by SBI.

Go Live as CSP: After completing the training and infrastructure setup, you can start offering SBI banking services to customers through your CSP. Adhere to the operational guidelines provided by the bank and maintain compliance with the necessary regulations.

Please note that the exact registration process and requirements may vary based on SBI’s policies and guidelines. It is recommended to directly contact the bank or visit the nearest SBI branch for detailed information and guidance on the CSP registration process.

As an SBI CSP (Customer Service Point), you will be authorized to provide various banking services on behalf of State Bank of India. These services aim to extend the reach of SBI’s banking facilities to unbanked or underbanked areas, promoting financial inclusion. Here are some of the common services that you can offer as an SBI CSP:

Account Opening: You can assist individuals in opening SBI savings accounts, current accounts, and other types of accounts offered by the bank. This includes helping customers fill out the necessary application forms and verifying their identity and address proofs.

Cash Deposits and Withdrawals: Customers can deposit and withdraw cash through your CSP. You will be responsible for accepting cash deposits into their SBI accounts and providing cash withdrawals as per their requirements.

Fund Transfers: You can facilitate various fund transfer services, such as transferring money between SBI accounts, interbank transfers, and remittance services. This allows customers to send and receive money securely.

Balance Inquiries and Mini-Statements: As an SBI CSP, you can provide customers with account balance inquiries and mini-statements. This enables them to check their account balances and review recent transactions.

Bill Payments: You can assist customers in paying their utility bills, such as electricity, water, gas, and telephone bills, using their SBI accounts. This service helps individuals conveniently settle their bills through your CSP.

Aadhaar Enabled Payment System (AEPS): SBI CSPs often offer AEPS services, allowing customers to perform banking transactions using their Aadhaar card details. This includes services like cash withdrawals, balance inquiries, and Aadhaar-to-Aadhaar fund transfers.

Government Schemes and Benefits: SBI CSPs can facilitate the disbursement of various government subsidies, pensions, and other financial benefits. This helps individuals receive their entitlements directly into their SBI accounts.

Loan Applications and Repayments: You may assist customers in applying for SBI loans and provide guidance throughout the loan application process. Additionally, you can accept loan repayments on behalf of the bank.

Insurance and Investment Products: Depending on the specific agreement with SBI, you may have the option to offer insurance and investment products provided by the bank. This can include selling insurance policies, mutual funds, fixed deposits, and other investment options.

As an SBI CSP, it is important to follow the guidelines and operating procedures set by the bank. You will be representing SBI and should maintain professionalism, integrity, and compliance with banking regulations.

Please note that the availability of services may vary based on the specific CSP agreement with SBI and the infrastructure capabilities of your CSP location. It is recommended to directly contact SBI or visit the nearest SBI branch for detailed information on the specific services you can offer as an SBI CSP.